Funding for Manufacturing

Manufacturing Invoice Funding to Keep Production Moving

Manufacturing invoice funding helps manufacturers access capital tied up in unpaid invoices so they can keep production running, purchase materials, and fulfill larger orders without waiting on net 30, 45, or 60+ day payment terms.

4.8/5 Average Partner Rating on Google

Does Invoice Funding Make Sense for Your Manufacturing Business?

Running a manufacturing business means cash is always moving in two directions, no matter what you’re producing.

Money goes out first. Raw materials need to be purchased, production has to be scheduled, and labor costs show up before a single dollar from the order comes back in. Then, once the work is complete and delivered, payment is still on a timeline that you don’t control.

That timing mismatch is where things start to tighten.

You might notice it when:

- A larger order requires more upfront spend than usual

- Production schedules depend on when cash becomes available

- New opportunities feel exciting, but also come with hesitation

- Working capital starts dictating how much you can produce

None of that means the business isn’t performing. In many cases, it’s the opposite. Demand is there. Customers are ordering. The challenge is keeping everything funded while revenue is tied up in invoices.

For manufacturers that are actively producing and billing on terms, access to capital at the right time becomes just as important as the work itself.

That’s where invoice funding can come into play. It gives you a way to pull cash forward from completed orders so you can keep purchasing materials, running production, and accepting new work without constantly adjusting to payment timelines.

When your ability to produce is strong but your cash flow feels out of sync with it, that’s usually when this type of funding starts to make sense.

What Invoice Funding Means for Manufacturing Businesses

Invoice funding is a way for manufacturers to access cash from invoices that have already been issued but not yet paid.

After you complete a production run and bill your customer, that invoice becomes an asset on your books. The challenge is that it doesn’t turn into usable cash until your customer pays, which could be weeks and even months down the line.

Invoice funding allows you to convert 90% of that invoice into working capital much sooner.

You might also hear it referred to as:

- Invoice factoring

- Manufacturing factoring

- Accounts receivable financing

- A/R funding

- payroll funding

The terminology can vary depending on the structure, but the underlying idea is straightforward. You are using the value of completed work to access capital instead of waiting through the full payment cycle.

For manufacturers, this can change how cash moves through the business. Instead of having funds tied up in receivables while production continues, you’re able to put that capital back into materials, labor, and operations much earlier.

At its core, invoice funding is simply a way to turn finished work into usable cash without relying on when a customer decides to pay.

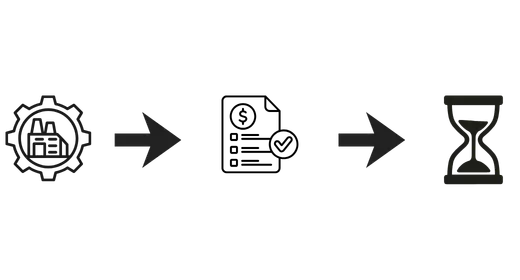

This is How Manufacturing Invoice Funding Works

In manufacturing, the timing of cash usually lags behind the work itself. Funding is structured to follow your production cycle so you’re not waiting on completed orders to turn into usable capital.

Here’s how that typically plays out:

1. Production is completed and the invoice is issued

You manufacture and deliver the product, then bill your customer based on your agreed terms. At this point, the work is finished, but the payment timeline is just beginning.

2. The invoice is submitted for funding

Once the invoice is submitted, it is quickly reviewed before funding.

3. Capital is advanced against the invoice

After approval, 90% of the invoice value is released to your business.

For example:

- Invoice amount: $60,000

- Upfront capital: $54,000

- Remaining balance held: $6,000 (10%)

That gives you immediate access to funds tied to work you’ve already completed.

4. Your customer pays according to terms

Your customer continues paying on their normal schedule. There’s no need to change how you bill or when they pay.

5. The remaining balance (10%) is released

Once the invoice is paid, the remaining portion is sent to your business, minus any fees.

The key difference is timing. Instead of production finishing and cash being delayed, you’re able to keep reinvesting into materials, labor, and output as soon as the work is done.

Why Manufacturers Often Choose Invoice Funding Over Traditional Options

For many manufacturers, the challenge isn’t finding financing. It’s finding financing that actually keeps up with how the business operates.

Traditional options like bank loans, lines of credit, and SBA programs are built around fixed limits and stricter approval processes. They can work well in stable situations, but manufacturing rarely stays static. Order sizes change, production cycles vary, and capital needs can shift quickly depending on demand.

That’s where things start to feel restrictive.

- A credit line might help cover part of your costs, but it doesn’t automatically expand just because you landed a larger order.

- A loan gives you a set amount upfront, but once it’s used, you’re back to managing within that same constraint.

Invoice funding works from a different starting point.

Instead of relying on a predetermined limit, it’s tied directly to the work your business is already completing. As you produce more and invoice more, the amount of available capital increases alongside it. That creates a more natural alignment between your operations and your access to funds.

There’s also a timing advantage.

Traditional financing requires asking for an increased line or a larger loan with the answer often being no. Invoice funding is based on completed work, which means it becomes available as your business continues to operate.

For manufacturers dealing with fluctuating order sizes and ongoing production demands, having funding that adjusts with activity rather than staying fixed can make day-to-day decisions much easier.

When Invoice Funding Starts Making Sense for Manufacturers

For many manufacturers, the shift toward invoice funding doesn’t come from curiosity, it comes from pressure or opportunity.

On one side, you might be seeing more demand than ever. Larger orders, repeat customers increasing volume, or new accounts coming in faster than expected. Growth is happening, but each new order requires more materials, more labor, and more upfront cash before anything gets paid.

On the other side, you might start noticing friction in your day-to-day operations. Purchasing decisions get delayed. Production planning becomes more cautious. You find yourself thinking twice about taking on additional work, not because you can’t handle it, but because of what it will require financially before payment arrives.

That’s usually the point where funding becomes part of the conversation.

Invoice funding fits particularly well in situations like:

- Stepping into larger production runs that require more upfront investment

- Expanding output for existing customers

- Adding new clients while maintaining current commitments

- Wanting to move faster without constantly checking available cash

There’s also a longer-term consideration. Some manufacturers choose to support growth using their own capital, but that approach ties up funds that could be used elsewhere. Over time, that can limit flexibility more than expected.

With the right funding structure in place, you’re not forced to slow down when opportunity shows up. You’re able to keep production moving, take on additional work, and make decisions based on demand rather than cash timing.

What This Looks Like Inside a Manufacturing Operation

Picture a manufacturer that just secured a larger order from an existing client.

The order is a good one. Higher volume, better margins, and a chance to strengthen the relationship. The catch is everything that comes with it. More raw materials need to be purchased upfront. Production has to ramp up. Labor costs increase before anything is paid.

- The company completes the run and sends out a $75,000 invoice on net 45 terms.

- Now the business is in a familiar position. The work is done and the revenue is booked, but the cash is still tied up while the next round of production is already knocking on the door.

- Instead of slowing things down or dipping into reserves, the company uses invoice funding.

- At a 90 percent advance, they receive $67,500 upfront, with $7,500 (10%) held in reserve.

- That capital goes right back into the operation. Materials are ordered for the next batch. Production continues without interruption. The team stays focused on output instead of waiting on incoming payments.

- When the client pays the invoice, the remaining balance (10%) is released minus fees.

- From the outside, nothing changes. Orders are still fulfilled. Clients are still billed on the same terms. But internally, the business is running with far more flexibility, allowing it to take on more work without hesitation.

Ready to Keep Production Moving Without Waiting on Payments?

If your manufacturing business is growing, taking on larger orders, or feeling pressure from delayed payments, it may be time to look at invoice funding as a way to operate more efficiently.

Whether you are preparing to scale production, expand into new opportunities, or simply want more control over your cash flow, getting the right funding structure in place can make a meaningful difference.

We can help you understand your options and connect you with a funding partner that fits how your business operates and knows how manufacturing invoice funding works.

FAQS

Frequently Asked Questions About GovCon Funding

Manufacturers can typically access 90 percent of their invoices and receivables. This means there is technically no limit on how much funding a manufacturing company can recieeve. The more they are billing their end clients, the more they can access.

Nope, your customers can continue to pay on the same terms they always have. Invoice funding is designed to work with how your business already operates.

The timeline depends on documentation collection, but many manufacturers are able to get set up and begin accessing capital within a relatively short timeframe once everything is in place.

Yes. Many manufacturers use invoice funding specifically to take on larger orders. It allows you to access capital from completed work so you can reinvest into materials, labor, and production without slowing down.

Not necessarily. Invoice funding can work alongside existing financing. Some businesses use it as a primary source of working capital, while others use it to supplement their current setup and create more flexibility.

No. Manufacturing is a strong fit, but we also work with businesses in staffing, government contracting, construction, and other industries that operate on net terms.