Invoice Factoring and Receivables Financing

Invoice Factoring for Businesses Waiting on Customer Payments

GetInvoiceFunding helps B2B companies compare invoice factoring options and connect with funding partners that understand their industry, receivables and cash-flow needs.

4.8/5 Average Partner Rating on Google

Find the Right Invoice Factoring Partner for Your Business

We help businesses that bill on net terms get invoice factoring from both sides: understanding how it works and comparing options that fit their industry, customer base and payment cycle. Instead of sorting through providers alone, you can review your situation with a partner who helps make the structure clearer before you move forward.

This is especially relevant for companies in staffing, government contracting, security, transportation, manufacturing, construction, home care, janitorial, IT and consulting, where payroll, materials, project costs or operating expenses often come due before customers pay.

The goal is simple: help you understand whether eligible invoices can support working capital, what the structure may cost, and which funding partner is most likely to fit the way your business actually operates.

Already have a factoring proposal, renewal offer or funding agreement? Start with an invoice factoring rate review before you sign, renew or switch providers.

Built for Businesses That Operate on Net Terms

Invoice factoring is built for businesses that complete work, send invoices and wait for customers to pay. The company may be healthy, growing and billing real revenue, but cash can still feel tight when receivables sit open for weeks.

That timing gap matters most when expenses arrive before collections. Payroll, contractor payments, fuel, materials, insurance, software and operating costs may all need to be covered while invoices are still moving through the customer’s payment process.

This is especially relevant for companies that:

- Bill commercial, government or enterprise customers on terms

- Wait 30, 45, 60 or more days after invoices are sent

- Need working capital for payroll, materials, contractors or operations

- Have receivables from customers with reliable payment history

- Want to take on more work without waiting for older invoices to clear

When revenue is sitting in accounts receivable, factoring may help convert eligible invoices into cash that can be used for current business needs instead of waiting for the full payment cycle to finish.

How Invoice Factoring Works at a High Level

The process usually begins after your business completes work and sends an invoice to a customer. Funding availability depends on eligible receivables, customer quality, invoice volume, concentration and approval from the funding provider.

1. Your business completes the work and invoices the customer

2. Eligible invoices are submitted for review

3. Your funder advances a percentage of the approved invoice

4. Your customer pays according to the payment instructions

5. The remaining reserve is released after payment, minus the agreed funding cost

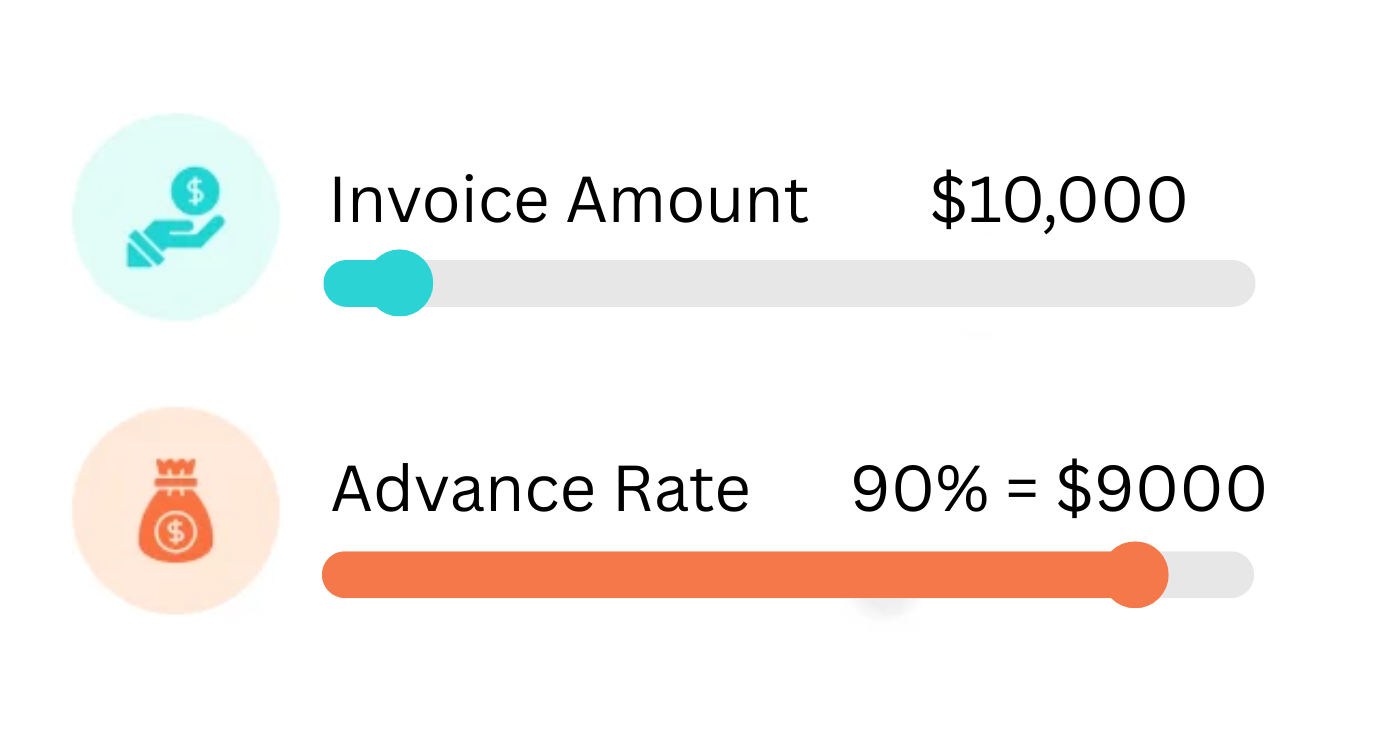

For example, if your company submits a $25,000 eligible invoice and is approved for a 90% advance, you would receive $22,500 upfront. The remaining $2,500 would be held in reserve and released after the customer pays, minus any agreed funding cost.

This allows your business to access capital without waiting through long payment cycles, making it easier to keep operations moving and support growth.

Compare Options Without Sorting Through Funders Alone

Finding the right factoring company is not just about getting approved. The structure, rate, advance percentage, customer experience and industry fit all matter.

GetInvoiceFunding helps narrow the search by connecting you with a trusted group of funding partners instead of forcing you to contact provider after provider on your own. The goal is to help you understand your options, compare the fit and move forward with a structure that makes sense for your receivables and business model.

If you already have an offer, the rate review process can also help you evaluate whether the proposal is competitive before you sign, renew or switch.

Explore Invoice Factoring by Industry

Different industries use factoring for different reasons. Staffing firms may need payroll support, manufacturers may need cash for materials, transportation companies may need fuel and driver pay, and consulting firms may need working capital while client invoices move through approval.

Explore the industries below to see how invoice factoring, invoice financing and receivables-based working capital may apply to your business.

Staffing

Staffing firms can use staffing invoice financing to cover weekly payroll, onboard workers and support new client orders while invoices remain unpaid.

Government Contracting (GovCon)

Government contractors can use government contractor invoice factoring to support payroll, contract performance and operating costs while approved public-sector invoices move through payment.

Home Care

Home care agencies can use home care factoring to cover caregiver payroll, accept new cases and maintain care schedules while waiting on payer or client payments.

Security

Security companies can use security company invoice factoring to pay guards, expand coverage and support new contracts while customer invoices are still open.

Information Technology (IT)

IT service providers can use IT invoice financing to support technical teams, contractors, software costs and client delivery while invoices are paid on terms.

Manufacturing and Distribution

Manufacturers can use manufacturing invoice factoring to support materials, labor, production costs and upcoming orders while customer invoices are still unpaid.

Janitorial

Cleaning and facility service companies can use janitorial invoice factoring to cover payroll, supplies and recurring contract costs while waiting on monthly client payments.

Construction

Contractors can use construction invoice factoring to support labor, materials and project costs while approved invoices move through customer payment cycles.

Consulting

Consulting firms can use consulting invoice factoring to cover payroll, subcontractors, software and new client work while waiting on approved invoices.

Trucking & Logistics

Freight and logistics companies can use trucking invoice financing to cover fuel, driver pay and operating costs while broker, shipper or customer invoices remain unpaid.

Ready to Compare Invoice Factoring Options?

If your business is growing, taking on larger customers or feeling pressure from unpaid invoices, the right factoring structure may help turn receivables into usable working capital.

Share a few details about your business, customers and open invoices. We can help you review options and connect with a funding partner that fits your industry and receivable profile.

FAQS

Common Questions About Invoice Factoring

Invoice factoring is a receivables-based financing option where a business receives an advance against eligible unpaid invoices. Instead of waiting for the customer to complete payment, the business can access a portion of the invoice value sooner and use it for payroll, materials, operations or growth.

Availability depends on eligible invoice volume, customer quality, payment history, receivable concentration and approval from the funding provider. As approved receivables grow, available working capital may also increase.

Timing depends on underwriting, documentation, and end customer review. After a facility is approved and set up, individual invoices can typically be funded within 24 hours.

Costs vary based on industry, invoice volume, customer quality, payment speed, advance rate and the funding structure. A lower headline rate is not always the full story, so it is worth reviewing the full proposal before signing. You can also request an invoice factoring rate review if you already have an offer.

It depends on the business. A loan is usually based on borrowing capacity and repayment terms, while factoring is tied to eligible receivables. Factoring may be useful for companies that have strong customer invoices but need cash before those invoices are paid.

Not always. Many factoring providers place more weight on your customers’ ability to pay than on personal credit alone. Your company’s financials, receivables, customer base and existing obligations can still affect approval and structure.