Receivables Financing for Manufacturers

Manufacturing Invoice Factoring for Materials and Production

Finished goods may already be delivered while the cash needed for raw materials, payroll and the next production run remains tied up in customer invoices. Manufacturing invoice factoring helps convert eligible receivables into working capital before net 30, 45 or 60+ day payment terms are complete.

4.8/5 Average Partner Rating on Google

Is Invoice Factoring Right for Your Manufacturing Business?

Manufacturers often commit cash well before customer payment arrives. Raw materials must be ordered, employees and machine operators must be paid, equipment must stay running and packaging or freight costs may be due before the finished goods invoice is collected.

The pressure becomes more noticeable when order volume increases faster than accounts receivable turns into cash.

You might notice it when:

- A larger order requires more raw materials or production labor upfront

- Supplier payments are due before customer invoices are collected

- Production schedules are being delayed because cash is tied up in receivables

- Overtime, temporary labor or additional shifts are needed to meet demand

- One major customer represents a large share of outstanding invoices

- Available working capital is limiting the size or number of orders you can accept

Manufacturing invoice factoring may help when completed and delivered orders have created valid receivables, but customer payment terms are preventing that cash from being reused for materials, labor or the next production run.

What Qualifies for Manufacturing Invoice Factoring

Manufacturing invoices are generally strongest candidates for factoring when the goods have been completed, delivered and accepted by a creditworthy commercial customer. The invoice should represent completed work, have clear payment terms and not be subject to unresolved disputes, returns or performance issues.

Eligibility may also depend on the customer’s payment history, the age of the invoice, the amount owed and how concentrated your receivables are among a small number of buyers. In most cases, the funding provider is evaluating the quality of the receivable and the customer responsible for paying it—not only the manufacturer’s credit profile.

You may also hear this called manufacturing factoring, accounts receivable financing, A/R financing or manufacturing invoice financing, depending on the provider and structure.

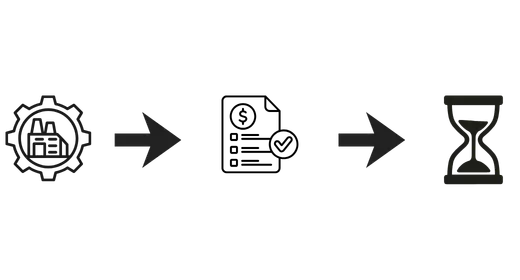

From Finished Order to Funded Receivable

The factoring process begins after the goods have been completed, delivered and billed. The funding provider may review the purchase documentation, delivery confirmation, invoice, customer and any acceptance requirements before determining whether the receivable is eligible.

Here’s how that typically plays out:

1. Production is completed and the invoice is issued

Your company completes the order, delivers the goods and invoices the customer according to the agreed commercial terms.

2. The receivable is reviewed

Your funding partner reviews the customer, invoice, delivery status and supporting documentation before approving the receivable.

3. Capital is advanced against the invoice

After approval, your funder advances 90% of the eligible invoice value.

For example:

- Invoice amount: $60,000

- Upfront capital: $54,000

- Remaining balance held: $6,000 (10%)

4. Your customer pays according to terms

The customer pays according to the applicable terms and payment instructions established through the factoring arrangement.

5. The remaining balance (10%) is released

After the customer pays, the remaining 10% reserve is released to your company minus the agreed funding cost.

Why a Fixed Credit Line Can Fall Behind Rising Order Volume

A manufacturer may have enough credit for normal production but not enough for an unusually large order, seasonal increase or new customer program. Banks often evaluate historical performance, collateral and fixed borrowing limits, while material and labor requirements can change quickly with order volume.

- An existing line may not increase quickly enough to support a larger production run

- A term loan provides a fixed amount that may not track changing invoice volume

- Equipment financing may help purchase machinery but not cover everyday materials or payroll

- Purchase order financing may apply before production, while invoice factoring applies after delivery and billing

Manufacturing invoice factoring is tied to eligible receivables rather than only a fixed loan amount. As approved invoice volume increases, funding availability may also increase, subject to customer quality, concentration limits and the terms of the facility.

A low-cost bank line may still be the better option when it is large enough and already available. Factoring becomes more relevant when receivables are growing faster than the company’s existing working-capital capacity.

When a Larger Order Creates a Working-Capital Gap

A large order can be profitable and still create a cash shortage. More units may require additional raw materials, overtime, temporary labor, packaging or supplier deposits before the customer pays for the finished goods. The company has the capacity and demand, but not enough free cash to support the full production cycle comfortably.

Invoice factoring fits particularly well in situations like:

- Increasing output for a major customer or distributor

- Purchasing raw materials for a larger production run

- Paying overtime or temporary labor during a demand spike

- Keeping suppliers current while customer invoices remain open

- Accepting a new account without delaying existing orders

- Covering packaging, warehousing or shipping costs after production

Factoring eligible receivables can preserve internal cash for equipment maintenance, product development, supplier deposits or unexpected production costs.

Manufacturing Work Where Cash Gets Tied Up Before Payment

Manufacturing companies often spend money long before customer payments arrive. Raw materials, labor, packaging, equipment, production runs and shipping costs may all come due while invoices are still waiting to be paid. That timing can create pressure even when the orders are strong and the customer relationship is solid.

Cash-flow pressure varies by manufacturing model. Machine shops may purchase metal or components before a customer pays. Contract manufacturers may add labor for a larger production run, while packaging and assembly businesses can complete and ship finished orders weeks before collection. Manufacturers selling to agencies or public-sector buyers may also want to review government contractor invoice factoring when approved government receivables move through longer payment cycles.

Production also depends on suppliers and service providers outside the plant. Manufacturers that ship finished goods through carriers may face related timing issues addressed through trucking invoice factoring. Companies using temporary machine operators, warehouse workers or assembly labor during demand spikes may also benefit from staffing invoice financing when payroll is due before customer invoices are collected.

Different manufacturing businesses carry different cost structures, but receivable delays can affect the same decisions: how much material to order, how many shifts to schedule and whether the next order can enter production on time.

Use Finished Orders to Support the Next Production Run

If your company has delivered finished goods and is waiting on creditworthy commercial customers to pay, those receivables may be able to support working capital for materials, payroll and upcoming orders.

Share a few details about your customers, invoices and production needs to compare factoring and receivables financing options.

FAQS

Manufacturing Invoice Factoring FAQs

The amount depends on eligible invoices, customer quality, billing volume, customer concentration and approval from the funding provider. A smaller manufacturer may only need enough availability for materials and payroll, while a larger company may require substantially more as receivables and order volume grow. Higher approved invoice volume can generally support higher funding availability.

The underlying payment terms may remain the same, but customers may receive a notice of assignment or updated remittance instructions directing payment to the factor. The exact process depends on the factoring arrangement.

Timing depends on the company’s financial information, customer details, invoice documentation and any liens or existing financing arrangements. Initial setup usually requires more review than funding an invoice after the factoring facility is already established.

Yes. Manufacturing invoice factoring can provide working capital from eligible invoices tied to completed and delivered orders. That cash can then be used for materials, payroll, production costs, shipping and other expenses connected to upcoming work.

Not necessarily. Manufacturing invoice factoring may supplement an existing bank line, equipment facility or other source of working capital. Any current lender, lien or borrowing agreement will need to be reviewed because it may affect how a factoring facility can be structured.

Manufacturing invoice factoring can apply to eligible B2B invoices from completed and delivered orders. This may include receivables from machine shops, contract manufacturers, metal fabricators, packaging companies, plastics manufacturers, food producers, assembly operations and other manufacturers selling to commercial customers. Approval depends on factors such as customer creditworthiness, invoice age, supporting documentation and whether the receivable is free from disputes.